US Market Concentration Risk: What It Means and What Canadian Investors Should Do

Is the US Stock Market Too Concentrated?

What Is Market Concentration Risk?

Why Has US Market Concentration Increased?

Why Investors Worry About Concentration

Does High Market Concentration Predict a Crash?

The Most Common Misinterpretation

Should Investors Reduce US Exposure Because of Concentration?

Will Today’s Largest Companies Stay Dominant?

Annual returns across global markets vary unpredictably

Market leadership changes frequently. Diversification allows investors to participate in global returns without relying on forecasts or persistent winners.

Why Sector Avoidance Usually Fails

Why Does Global Diversification Help With Concentration Risk?

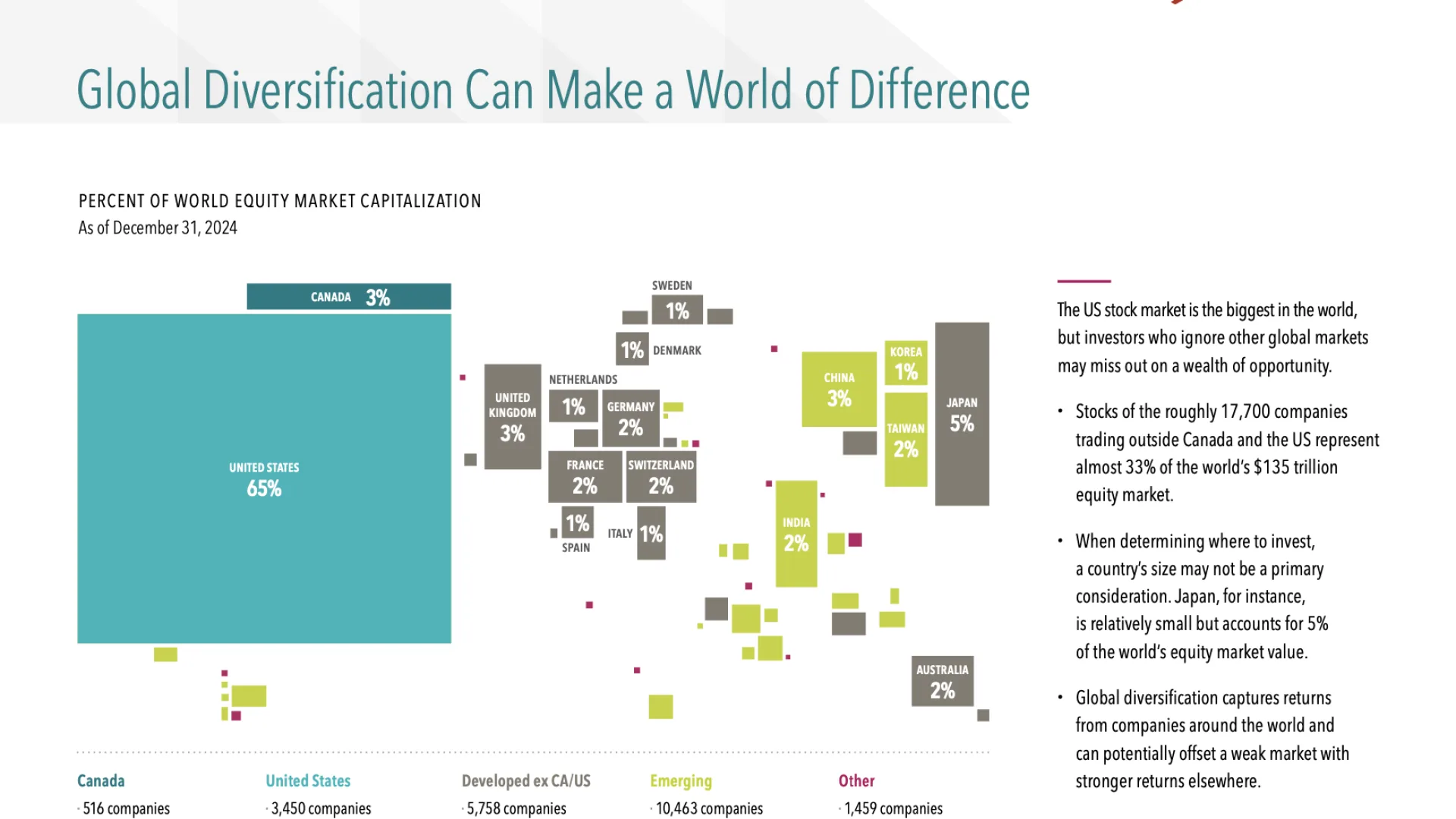

Global equity market capitalization by region

Market concentration levels vary across countries and regions. Global diversification reduces dependence on any single market or group of companies.

Does High US Concentration Mean Investors Should Take Action?

The Behavioural Risk Hidden Inside Concentration Fear

A Research-Driven Perspective on Concentration

What Canadian Investors Should Focus On Instead

FAQ: US Market Concentration & Diversification

Natural Closing

About Shea Sanche

Common Questions About This Topic

How do financial advisors in Canada get paid?

Common models include AUM fees, fee-for-service, commissions, or blended arrangements. What matters is understanding incentives and whether you receive coordination beyond investments.

What is a normal advisor fee in Canada?

Fees vary by service and complexity. Instead of comparing a single percentage, evaluate what the fee includes: planning outputs, coordination, accountability, and improved net outcomes.

Are financial advisors worth it in Canada?

They can be when the relationship coordinates investments, tax, estate, and decisions as a system. They are less valuable when the service is limited to reporting and portfolio-only management.