What History Teaches Us About New-Year Market Predictions

For me, the beginning of a new year always brings a renewed sense of optimism. It’s a time to reflect on goals, establish new routines, and plan for the year ahead. Personally, that means sticking to my goal of doing something active every day. Whether it’s a morning walk or staying consistent with my gym routine, it’s a habit that I notice improves my overall happiness and energy.

And as we turn the page on 2025, investors tend to do the same as they reflect on what’s happened and begin to forecast what’s to come. This is natural, as we all want to orient our sails correctly and take advantage of what’s to come. We aren’t alone in this desire, as some of the brightest minds on Wall Street shout their 2026 stock market predictions from the proverbial rooftops.

A Look Back at 2025

2025 was a spectacular year in the stock market, as we’ve enjoyed. The S&P 500 Index closed the year at approximately 6,845, up from about 5,980 at the start of the year—reflecting a price return of roughly 16%. What makes this worth noting is how the year unfolded. Between February and April, the market experienced a sharp pullback of more than 15%, largely driven by concerns around tariffs and global trade. Despite that volatility, markets recovered and finished the year solidly higher. This pattern of short-term discomfort followed by longer-term growth is far more common than it often feels in the moment.

Turning to 2026: Forecasts Everywhere

As we move into 2026, major institutional firms have once again published their outlooks for the S&P 500. Forecasts for the year range widely, from as conservative as +3.5% to well over +18%.

Spoiler alert: we’ll look into the accuracy of such prophecies later in this blog.

Source: Stock markets: Brokerage forecasts for S&P 500, global GDP

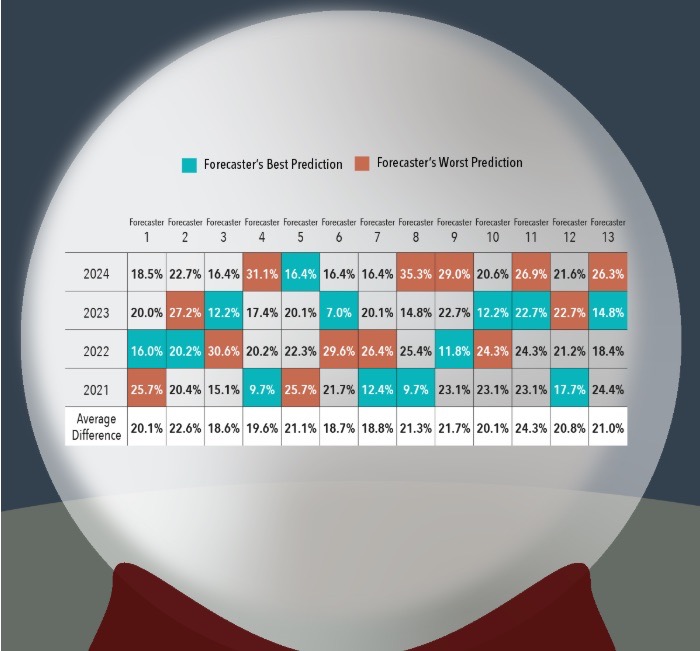

At a high level, analysts generally agree on a positive year ahead. However, it’s important to take these predictions with a grain of salt. When we look at historical accuracy of such predictions, forecasts have often missed the mark by wide margins. Bloomberg analyzed 13 equity analyst predictions for the S&P 500 over the past 5 years and found that these analysts were off by an average of over 20%! Even the most accurate forecaster was still off by an average of 18.6%. The takeaway isn’t that analysts lack insight, it’s that markets are simply very difficult to predict over short periods of time.

Difference Between Equity Analyst Forecasts and S&P Index Calendar-Year Returns

Source: When the Crystal Ball Is a Little Cloudy | Dimensional

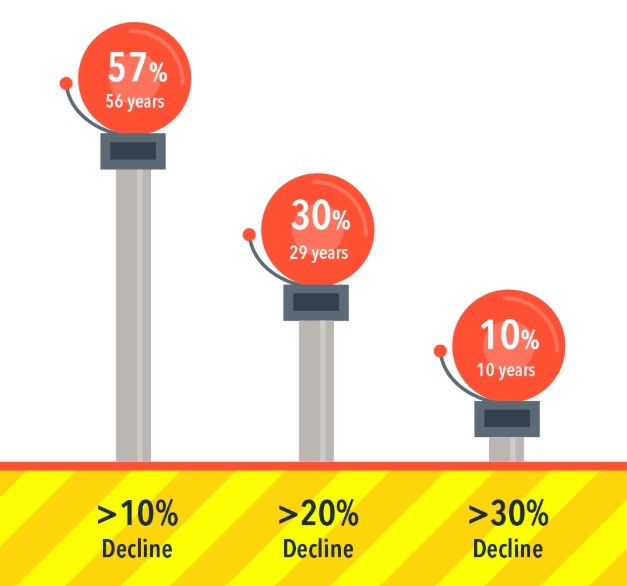

Over time, disciplined investors have come to accept a key reality: no one has a crystal ball. Calendar-year returns are influenced by unexpected events that can’t be forecast in advance. That realization isn’t pessimistic. It simply allows us to reframe our thinking and tune out the noise. The truth is that market pullbacks are a normal part of investing. In fact, a decline of 10% or more has occurred in 57% of calendar years since 1927. A decline of 20% or more has occurred in roughly 30% of calendar years. Importantly, a sharp decline during the year does not necessarily mean a negative year overall. Of the 29 years that experienced a decline of 20% or more at some point, only 6 ended the year still negative. In many cases, markets recovered (and sometimes significantly) before year-end.

Frequency of Declines in the US Stock Market, 1927 - 2024

Source: Stop, Drop, and Stay the Course | Dimensional

Just like building better habits takes time, successful investing rewards consistency more than perfection. Staying focused on the long term allows short-term noise to fade into the background. A new year is a great time for reflection, not reinvention. If you have questions about how your plan is positioned for the year ahead, I’m always here to help!

Common Questions About This Topic

How do financial advisors in Canada get paid?

Common models include AUM fees, fee-for-service, commissions, or blended arrangements. What matters is understanding incentives and whether you receive coordination beyond investments.

What is a normal advisor fee in Canada?

Fees vary by service and complexity. Instead of comparing a single percentage, evaluate what the fee includes: planning outputs, coordination, accountability, and improved net outcomes.

Are financial advisors worth it in Canada?

They can be when the relationship coordinates investments, tax, estate, and decisions as a system. They are less valuable when the service is limited to reporting and portfolio-only management.